LONDON/HOUSTON/SINGAPORE, Mar 10 – With 15 million barrels per day of Gulf supply suddenly offline, global oil demand will need to fall to rebalance the market—a process that could require prices to reach $150/bbl, according to new Wood Mackenzie analysis.

The scale of disruption is unprecedented. Gulf countries in total produce 20 million b/d of liquids, and 15 million b/d of exports have been taken out of the global market. The industry has never faced a loss of supply volumes of this magnitude.

“When the conflict ends, cranking up the supply chain won’t be swift,” said Simon Flowers, Chairman and Chief Analyst at Wood Mackenzie. “Product barrels in storage at refineries or in port might be moved on vessels quite quickly. But if wells are shut-in for a prolonged period, restarting production to full output could take weeks or even longer.”

Prices already $100/bbl

Competition for remaining barrels has already pushed prices above $100/bbl early this week. Markets dependent on exports have been particularly exposed across multiple regions.

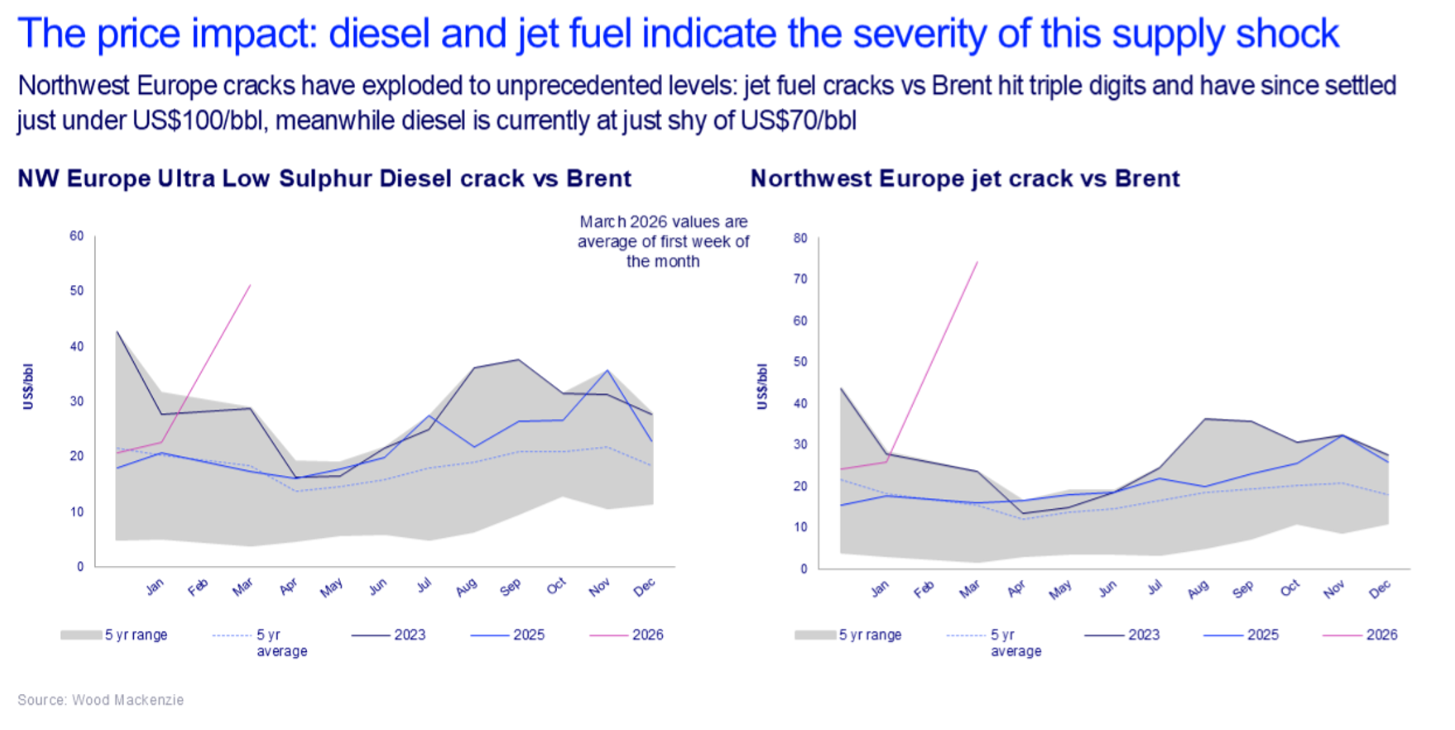

Europe faces especially acute challenges. In 2025, Gulf refineries supplied 60% of Europe’s jet fuel and 30% of its diesel, volumes which are now entirely cut off. Asia, which receives the majority of Gulf crude exports, faces equally severe pressure. Chinese, Indian, and other Asian buyers have been scrambling to secure alternative cargoes, driving up prices for West African and Latin American crude. Competition between Europe and Asia for limited non-Gulf supplies is intensifying price pressure across all regions.

The prospect of extreme tightness in refined product markets is reflected in super-high crack spreads. Jet-fuel cracks in NW Europe have traded at US$100/bbl (implying close to US$200/bbl Brent) and diesel cracks US$70/bbl, four to five times pre-war levels.

Strategic stocks and alternative supply offer limited relief

Strategic petroleum reserves offer some relief but cannot fully offset the supply loss. IEA member countries hold stocks equivalent to 90 days of imports, but sustained releases are unprecedented and IEA members account for less than half of global demand. During the Russia/Ukraine crisis, strategic stock releases did little to prevent prices reaching $125/bbl, and the supply gap from the Gulf shutdown is significantly larger.

Alternative supply sources also cannot fill the gap. While higher prices could incentivize US producers to accelerate output and forego maintenance, the Lower 48 could add only a few hundred thousand barrels per day over three to six months—a fraction of the 15 million b/d shortfall. With no supply solution available, demand destruction becomes the only rebalancing mechanism.

$150/bbl needed to rebalance

Prices will continue to escalate as the conflict prolongs, according to Wood Mackenzie analysis.

“Much will depend on how long the war lasts, how long the Strait of Hormuz remains closed and if the US Navy can ensure safe passage of vessels by escorting shipping,” said Flowers. “Global oil demand of 105 million b/d will still have to fall to balance the market and in our view, that will require Brent to push up at least to US$150/bbl in the coming weeks.”

At this price level, demand would fall through multiple channels: industrial users curtailing consumption, transport substitution away from oil-intensive modes, economic contraction reducing overall activity, and consumers reducing discretionary travel.

$200/bbl possible if conflict extends

While oil reached $150/bbl in inflation-adjusted terms during the 2022 Russia/Ukraine crisis, this situation could prove more severe.

“Supply volumes at risk this time are dimensionally bigger—and real,” said Flowers. “In our view, US$200/bbl is not outside the realms of possibility in 2026.”

No Responses